The EU Omnibus Package | Why Sustainability Still Matters

After weeks of speculation, the EU Commission’s proposed omnibus changes to the CSRD, CSDDD and EU Taxonomy have now been announced. Corporate sustainability advocates and many in civil society will be disappointed but not surprised.

The results of the Commission’s review are a significant rollback on the EU’s leadership on sustainability issues globally, rather than just a streamlining of reporting obligations, as had been suggested. The omnibus changes target key principles of the CSRD, CSDDD, and EU Taxonomy like upstream due diligence, while considerably restricting the overall set of companies impacted by the legislation, overturning years of effort and deliberation about the importance of integrating sustainability into business.

Set against a general global push toward deregulation, what do these fundamental alterations to the cornerstones of the EU Green Deal mean for due diligence and sustainability in business? In this article the TDi team consider the key changes proposed in the omnibus package and examine why sustainability not only still matters but is essential to long-term business productivity and resilience.

Background

Yesterday’s changes followed the November 2024 announcement by Ursula von der Leyen, President of the European Commission, of her intention to reduce the regulatory burden imposed on businesses through an omnibus bill addressing the CSRD, CSDDD and EU Taxonomy. The EU Commission framed the omnibus as a necessary step to recalibrate EU rules to enable more cost-effective delivery of policy objectives – building on the recommendations of the Draghi report and EU’s Competitiveness Compass to boost growth.

The proposed changes will now be submitted to the EU Parliament and Council for approval. The EU Commission has requested that the package is treated with priority, in particular the proposals postponing disclosure requirements under the CSRD and the deadline for transposition into national law under the CSDDD.

The CSRD, CSDDD and EU Taxonomy are key elements of the 2019 European Green Deal, meant to put the EU’s commitment to climate neutrality by 2050 into action by complying with the climate requirements of the Paris Agreement.

The EU Taxonomy for Sustainable Activities (2020)

Creates a classification system for businesses and investors to know what activities are considered green or climate friendly.

The Corporate Sustainability Reporting Directive (CSRD) (2023)

Created requirements for businesses to report greenhouse gas emissions and ESG actions. The CSRD requires reporting using the European Sustainability Reporting Standards (ESRS).

The Corporate Sustainability Due Diligence Directive (CSDDD) (2024)

Created additional reporting requirements and legal liability for companies in relation to their supply chains to ensure their suppliers comply with ESG goals.

What are the key changes announced yesterday?

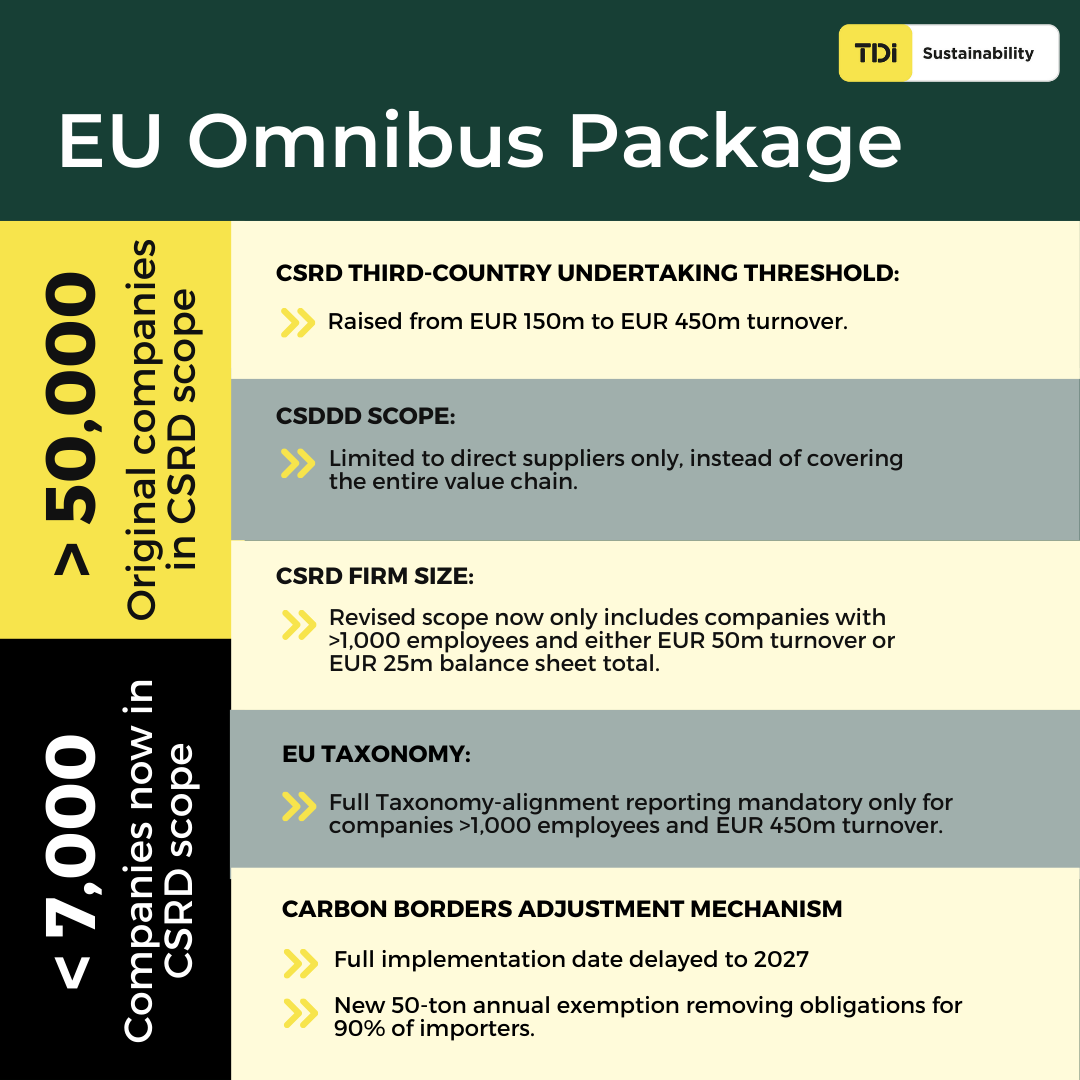

- Around 80% of companies have been removed from the CSRD’s scope with reporting requirements limited to the largest companies. In keeping with the CSDDD, companies with up to 1000 employees and less than 50 million turnover are out of scope.

- For the CSDDD, the due diligence focus is now only on direct business partners, rather than upstream value chain activities.

- Reporting has been postponed to 2028 for companies previously required to report in 2026 and 2027.

- For the Taxonomy, reporting is now mandatory only for “very large companies” – in line with the CSRD and the CSDDD changes.

- For companies in scope, the Commission will adopt a delegated act to revise and simplify the existing sustainability reporting standards

- An option has been introduced to report on activities that are partially aligned with the EU Taxonomy, allowing a gradual transition of activities over time.

- The harmonised EU conditions for civil liability have been removed and Member State obligations regarding representative actions by trade unions or NGOs have been revoked. Instead, it will now be up to national law to define whether civil liability provisions override otherwise applicable rules of the third country where the harm occurs.

While these changes clearly mark a new tone and set new priorities in Brussels, the Commission has preserved some elements of the Green Deal. Importantly, the double materiality principle of the CSRD has not been changed. Companies that remain in scope will have to report about how sustainability risks affect their business, as well as about their own impact on people and the environment.

Where next for my business?

The aim of the proposed modifications to the CSRD and CSDDD is to subject companies to a sustainability due diligence framework that is less complex and costly and more harmonised. As TDi found during the review of the Conflict Minerals Regulation that we carried out for the Commission in 2023, the implementation of some of the far-reaching and forward-thinking sustainability legislation from Brussels has proven complex. However, it is unfortunate to see the Commission stripping the Green Deal of some of its key provisions rather than doubling down on support to companies in scope, empowering them to harness the supply chain knowledge and risk awareness these regulations promised, in order to build more resilient business.

Even though the anticipated compliance and reporting burden on companies has been avoided or substantially reduced, the reputation, supply surety and political risks to companies linked with human rights, climate change, environmental, governance, price volatility and geo-political issues remain. Regardless of the changes that were announced yesterday, over the last ten years, TDi has consistently seen that supply chain due diligence and the integration of sustainability thinking into strategy makes companies more resilient and competitive by enabling them to understand exposure to sourcing risk. In order to plan for the future, companies need to proactively understand and mitigate supply chain risks – the approach at the heart of the EU’s sustainability regulations. TDi has built its in-house expertise and online management tools to help our clients to understand and manage multiple types of supply chains risks and enable their businesses to navigate an uncertain future.

Large companies in scope of the revised CSRD and CSDDD:

Get in touch for a free 30-minute consultation to discuss what you need to do to get ready for the new deadlines. Ensuring readiness for the CSDDD and CSRD will also ensure that your company is well prepared for other emerging sustainability regulations and disclosure requirements. It can also help to improve corporate reputation and access to capital as stakeholders increasingly expect solid sustainability credentials.

SMEs:

Although you may now be out of scope for the CSRD and CSDDD, supply chain due diligence is still essential to understand your exposure to sourcing risk, increase your business’s future resilience and competitiveness, and meet stakeholder expectations around environmental and social impact.

Voluntary reporting can also help to provide access to sustainable financing opportunities, as well as improving your business’s preparedness for future regulations and voluntary sustainability standards. Get in touch for a free consultation to discuss how TDi can help you identify and mitigate risk in your supply chains.

Want to understand the impact of the omnibus package on your business? Get in touch with TDi.